Seller Financing Rental Property in Florida: 2026 Guide

Discover how seller financing rental property in Florida can unlock investment opportunities. Learn the benefits, requirements, and legal steps.

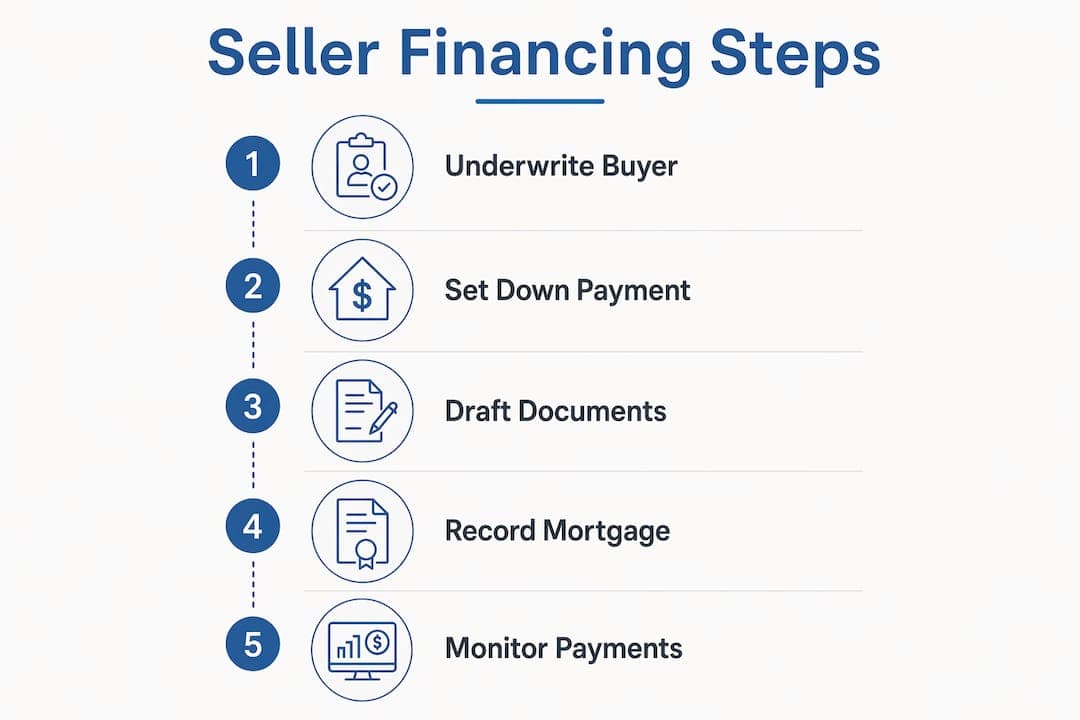

What are the legal requirements for seller financing rental property in Florida?

- — Collecting the buyer's tax returns, pay stubs, and bank statements to verify income

- Pulling a formal credit report and documenting the score on file

- Confirming the buyer's debt-to-income ratio supports the proposed payment

- Recording the promissory note and mortgage with the county clerk at closing

- Retaining all documentation in case of a future regulatory audit

Key Takeaways

- Down payment standard

- Require 15–20% down to protect seller equity and reduce

- Dodd-Frank compliance

- Use the one-property exemption correctly to avoid federal

- DSCR loan pairing

- Combine seller financing with DSCR loans to reduce upfront

- Tax trap awareness

- Check if existing mortgage balance exceeds adjusted basis

How to combine seller financing with DSCR loans for Florida rentals

- Step 1 — Identify the purchase price and target DSCR loan amount. Most DSCR lenders will fund 75–80% of the property's value Calculate the gap between that amount and the purchase price.

- Step 2 — Negotiate seller financing to cover part of the down payment. The seller carries a second position note for a portion of the remaining balance, reducing the cash you need at closing.

- Step 3 — Confirm the DSCR lender allows a seller-carried second. Not all lenders permit this Ask before you sign anything.

- Step 4 — Structure the seller's note with a balloon payment. A 3-to-5-year balloon gives you time to refinance once the property's value or your credit profile improves.

- Step 5 — Run the full debt service calculation. Add the DSCR loan payment and the seller note payment together, then divide by gross monthly rent The combined ratio must still satisfy the lender's threshold.

How to set up a seller financing deal step by step

- — A requirement that the buyer maintain hazard insurance naming the seller as additional insured

- — A clause requiring the buyer to pay property taxes on time, with the seller's right to pay and add to the note balance if the buyer defaults

- A maintenance standard requiring the property to remain in rentable condition

- A personal guarantee from the buyer if the buyer is purchasing through an LLC

What are the risks and pitfalls in Florida seller financing rental deals?

- — Tax traps from existing mortgages. If the outstanding mortgage balance exceeds the seller's adjusted tax basis, the IRS treats the excess as cash received in the year of sale, triggering immediate capital gains tax even if no cash changed hands. This surprises sellers who carry significant depreciation.

- — Rising insurance and property tax costs. Florida's insurance market has hardened significantly. Escalating insurance and local tax costs directly affect buyer cash flow and increase the probability of default on seller-financed notes.

- — Incomplete documentation. A promissory note without a recorded mortgage, or a deal structured without proper buyer underwriting, creates legal gaps that are expensive to fix after closing.

- — No personal guarantee. When a buyer purchases through an LLC and the seller does not require a personal guarantee, the seller's only recourse is the property itself. If the property value drops, the seller absorbs the loss.

Key Takeaways

Seller financing rental property in Florida works best when sellers underwrite buyers carefully, document every term in a recorded mortgage, and treat the promissory note as an active lending asset.

Seller financing rental property in Florida works best when sellers underwrite buyers carefully, document every term in a recorded mortgage, and treat the promissory note as an active lending asset.

What I have learned from watching seller financing deals go wrong

— Eric

What I have learned from watching seller financing deals go wrong

Seller financing looks simple on paper. The seller carries the note, the buyer makes payments, and everyone wins.

Seller financing looks simple on paper. The seller carries the note, the buyer makes payments, and everyone wins. The reality is messier, and the deals that fail almost always fail for the same reason: the seller treated the note like a passive investment.

The most underrated part of owner financing rental properties is deal sourcing. Searching the MLS for "owner will carry" listings reveals properties that banks have rejected for condition or title issues. Those are exactly the deals where seller financing makes sense, because the seller has no other exit. That leverage is real, and most investors never use it because they assume seller financing is rare.

The second mistake I see constantly is sellers skipping the personal guarantee when the buyer uses an LLC. An LLC limits the buyer's personal liability. Without a guarantee, the seller's only collateral is the property. If the buyer walks away and the property has declined in value, the seller takes the full loss. Always require the personal guarantee.

The third mistake is ignoring the Florida closing process and recording requirements. Sellers who close without recording the mortgage lose their lien priority. A subsequent creditor or lien holder can leapfrog an unrecorded seller mortgage. That is not a theoretical risk. It happens.

Persistence in negotiating seller financing uncovers deals that banks reject outright. Those deals often carry the best terms because the seller has no competing offers. The investors who close the most seller-financed deals are the ones who ask for it on every offer, not just the ones where it seems obvious.

How Housefastcashfl helps Florida sellers and investors move fast

Seller financing deals are complex. Not every seller wants to carry a note for five years, and not every property is the right fit for an installment sale structure.

Seller financing deals are complex. Not every seller wants to carry a note for five years, and not every property is the right fit for an installment sale structure. Sometimes the fastest and cleanest exit is a direct cash offer.

Housefastcashfl works with Florida property owners who need to move quickly, whether they are landlords exiting a rental portfolio, sellers facing foreclosure, or investors who want to close without the legal complexity of carrying a note. Housefastcashfl provides fair cash offers within 24 hours with closing timelines as short as four days, regardless of property condition. If you want to verify that the process is legitimate before you commit, the legitimacy and buyer verification page walks through exactly what to look for in a credible cash buyer. No commissions, no repairs, no waiting.

Free Cash Offer

Ready to sell your house for cash?

Tell us about your property. We'll come back within 24 hours with a fair, no-obligation cash offer — no commissions, no inspection drama, no closing-cost surprises.

- Licensed Florida cash buyer

- Close in 7-21 days, on your timeline

- Free, no-obligation cash offer

- We respond within 24 hours

Cash Buyers Network

Sources & References

External sources cited in this article. Verify current figures and rules directly with the issuing source — Florida real-estate data and program rules change quarterly.

From the Blog

Continue Reading

home-selling

Role of Heirs in Property Sales: 2026 Guide

Discover the role of heirs in property sales. Learn when you can sell inherited property and avoid common probate mistakes.

Read articlehome-selling

House Selling Timeline in 2026: What to Expect

Discover the key steps to explain house selling timeline 2026. Learn how to prepare and navigate the process for a successful sale.

Read articlehome-selling

Red Flags When Selling Property: 2026 Seller's Guide

Discover the red flags when selling property in 2026. Protect your equity and avoid pitfalls with our essential seller's guide!

Read articlehome-selling

Florida Landlord Tenant Law: Selling With Tenants

Learn about Florida landlord tenant law sale rules. Discover your legal obligations when selling tenant-occupied properties and protect yourself.

Read articleFrequently Asked

Common Questions

What is seller financing for a rental property in Florida?

+

Seller financing is a transaction where the property owner acts as the lender, accepting a promissory note secured by a mortgage instead of a lump-sum cash payment. The buyer makes monthly payments directly to the seller under agreed terms.

How much down payment does seller financing require in Florida?

+

Seller-financed deals in Florida typically require 15–20% down, which is often lower than the 20–25% required by traditional investment property lenders.

Does the Dodd-Frank Act apply to seller financing in Florida?

+

Yes. The Dodd-Frank Act applies to residential seller financing in Florida. Individual sellers can use the one-property exemption to finance one residential property per 12-month period without a federal mortgage originator license.

Can I combine seller financing with a DSCR loan on a Florida rental?

+

Yes. DSCR loans cover 75–80% of the property value, and a seller-carried second note can cover part of the remaining balance. Confirm the DSCR lender permits a seller second before structuring the deal.

What happens if a buyer defaults on a seller-financed note in Florida?

+

The seller must file a judicial foreclosure lawsuit to recover the property. Florida's foreclosure process typically takes 6–18 months and requires legal representation, making default prevention through proper underwriting the best protection.