Florida Closing Costs Explained: What Buyers and Sellers Pay

Curious about closing costs? This guide will explain closing costs in Florida for buyers and sellers, helping you budget for your real estate deal.

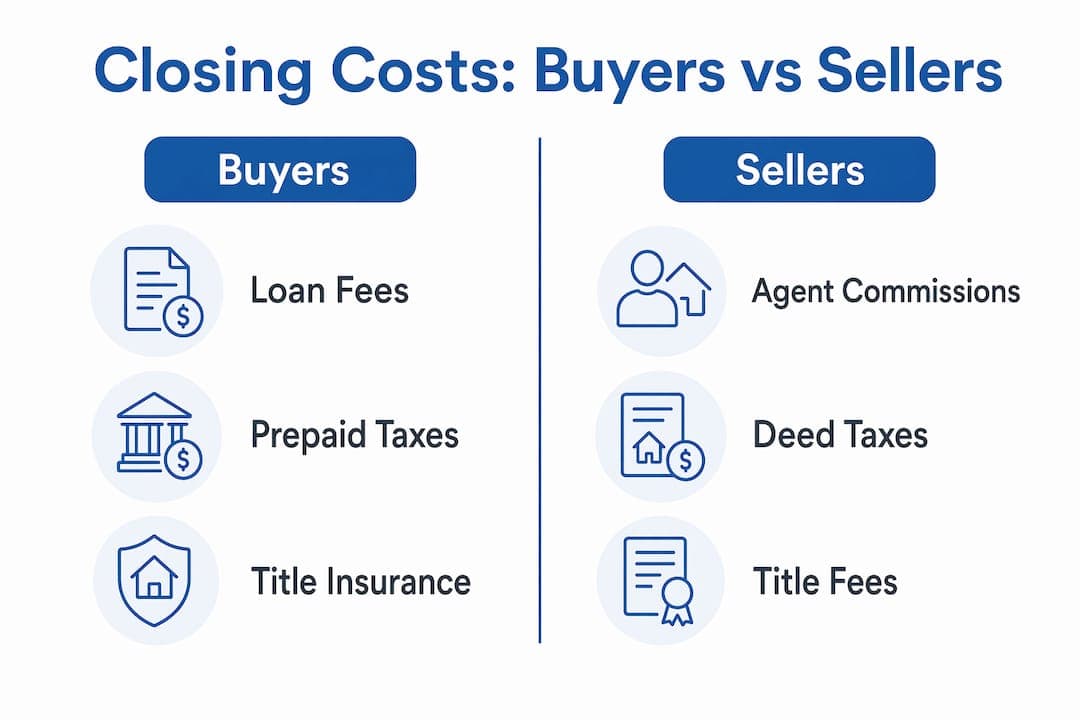

What are the main components of closing costs in Florida?

- — Documentary stamp tax on the deed: The seller typically pays this at $0.70 per $100 of the sale price. Miami-Dade County uses a lower base rate of $0.60 per $100 but adds a surtax on non-homestead properties.

- — Documentary stamp tax on the mortgage note: Financed buyers pay $0.35 per $100 of the loan amount to the state.

- — Intangible tax on the mortgage: Buyers with a mortgage pay 0.20% of the loan amount as an intangible tax. Cash buyers pay neither of these mortgage taxes.

- — Property tax prorations: Sellers credit buyers for the portion of the year they owned the property before closing.

- — Owner's title insurance: Protects the buyer against prior claims on the property. Who pays varies by county. Sellers pay in South Florida counties like Palm Beach, while buyers pay in Sarasota, Collier, and Lee counties.

Key Takeaways

- Down payment

- Your equity contribution, typically 3%–20% of the purchase

- Loan closing costs

- Origination, appraisal, title, and state taxes

- Prepaid homeowners insurance

- First year of coverage paid upfront to the insurer

- Initial escrow deposit

- Two to three months of property taxes and insurance held by

How does cash vs. mortgage financing change your closing costs?

- Step 1 — Cash purchase: No mortgage means no documentary stamp tax on a note, no intangible tax, no lender's title insurance, and no loan origination fee The buyer pays title fees, the deed tax credit from the seller, and any agreed-upon costs. Cash buyers may also receive a net credit at closing because sellers prorate property taxes, and the absence of mortgage taxes keeps total costs low.

- Step 2 — Financed purchase: The buyer pays all cash-purchase costs plus the documentary stamp tax on the mortgage note, the intangible tax, lender's title insurance, and all loan origination fees The lender passes these state-mandated taxes directly to the buyer at closing, even though the legal liability technically rests with the lender.

- Step 3 — FHA or VA loans: These government-backed loans carry their own fee structures, including FHA mortgage insurance premiums or VA funding fees, which add to the total.

- Step 4 — Prepaid escrow requirements: Lenders require financed buyers to fund an escrow account at closing for future property tax and insurance payments This escrow deposit can add several months of expenses to the upfront cash requirement.

What Florida-specific closing cost rules should you know?

- — Municipal lien search: This is a Florida-specific step that uncovers outstanding code violations or unpaid utility bills attached to the property. Without it, a buyer can inherit those liabilities after closing. The cost is modest, but skipping it is a serious financial risk.

- — County-specific title insurance customs: Florida has no statewide rule on who pays for owner's title insurance. The custom varies by county and is legally negotiable in every transaction. Review the local custom for your county before signing a contract, because the default assumption can shift thousands of dollars between buyer and seller.

- — Miami-Dade documentary stamp surtax: Properties in Miami-Dade that are not the buyer's primary residence carry an additional surtax on the deed transfer. This cost catches out-of-state investors and second-home buyers off guard regularly.

- — HOA and condo estoppel fees: If the property belongs to a homeowners association or condominium, the seller must obtain an estoppel letter confirming the current balance owed. Florida law caps the fee for this letter, but it is still a closing cost the seller must budget for.

- — Strategic closing date timing: Closing in the final week of the month reduces the number of prepaid interest days a buyer owes. Fewer days between closing and month-end means less cash due at the table.

How do you calculate the total cash you need at closing?

Closing costs and cash to close are not the same number. [Cash to close equals closing costs plus your down…

Closing costs and cash to close are not the same number. Cash to close equals closing costs plus your down payment, minus any earnest money already deposited, plus prorated taxes and HOA fees. Buyers who budget only for closing costs routinely arrive at the table short on funds.

The table below shows the main components that make up a buyer's total cash to close on a financed purchase:

Prepaid homeowners insurance and escrow deposits frequently add several thousand dollars to the total, which surprises buyers who focused only on the loan fees. The Closing Disclosure document, which your lender must provide three business days before closing, shows the final version of every number in this table. Review it line by line with your real estate attorney or agent before the closing date.

Pro Tip: Compare your Closing Disclosure to the original Loan Estimate you received at application. Any fee that increased significantly may be worth questioning with your lender before you wire funds.

What negotiation strategies reduce closing costs in Florida?

- — Seller concessions: You can ask the seller to contribute toward your closing costs as part of the purchase offer. This is common in buyer-friendly markets and reduces your upfront cash requirement without changing the purchase price.

- — Shop for settlement services: The Loan Estimate lists services you can shop for, including title companies and settlement agents. Comparing quotes from two or three title companies can reduce fees by a meaningful amount.

- — Negotiate title insurance responsibility: In counties where the custom is flexible, you can negotiate which party pays for owner's title insurance. This is one of the larger line items in a Florida closing and is worth addressing explicitly in the contract.

- — Choose your closing date wisely: Scheduling your closing in the last week of the month cuts prepaid interest costs. On a $400,000 loan, the difference between closing on the 5th versus the 28th can be several hundred dollars.

- — Work with experienced professionals: An experienced Florida real estate attorney or title agent knows the local customs, spots errors in the Closing Disclosure, and can flag fees that are duplicated or inflated. Their fee is a closing cost that pays for itself.

Key Takeaways

Florida closing costs range from 2%–5% for buyers and 6%–10% for sellers, with cash buyers paying the least and financed buyers carrying the heaviest tax burden.

Florida closing costs range from 2%–5% for buyers and 6%–10% for sellers, with cash buyers paying the least and financed buyers carrying the heaviest tax burden.

What I've learned watching buyers get blindsided at the closing table

— Eric

What I've learned watching buyers get blindsided at the closing table

After years of working through Florida real estate transactions, the pattern I see most often is not ignorance of closing costs.

After years of working through Florida real estate transactions, the pattern I see most often is not ignorance of closing costs. It is the gap between what buyers think they know and what the actual Closing Disclosure says. Most buyers understand that closing costs exist. Very few understand that prepaid escrow deposits and homeowners insurance can push their total cash to close well above their original estimate.

The municipal lien search is the single most overlooked item I encounter. Buyers focus on the inspection and the appraisal. They treat the lien search as a formality. Then they discover a $15,000 code violation the seller never disclosed, and the deal either collapses or the buyer absorbs the cost. That outcome is entirely preventable.

My advice is direct: read your Closing Disclosure three days before closing, not the morning of. If a number changed from your Loan Estimate, ask why before you wire funds. And if you are selling, understand that your net proceeds from the sale depend heavily on what you agreed to pay at closing. Negotiate every negotiable item in the contract, not after it is signed.

How Housefastcashfl simplifies closing for Florida sellers

Closing costs add up fast, especially for sellers managing commissions, deed taxes, and title fees on top of an already stressful sale.

Closing costs add up fast, especially for sellers managing commissions, deed taxes, and title fees on top of an already stressful sale.

Housefastcashfl offers Florida homeowners a direct path to a fast cash sale with no agent commissions, no repair costs, and a closing timeline as short as four days. You receive a no-obligation cash offer within 24 hours, and Housefastcashfl handles the closing process from start to finish. For sellers who want to skip the traditional cost structure entirely, this is a straightforward alternative. Learn more about selling your house fast or check whether cash home buying companies are legitimate before you decide.

Free Cash Offer

Ready to sell your house for cash?

Tell us about your property. We'll come back within 24 hours with a fair, no-obligation cash offer — no commissions, no inspection drama, no closing-cost surprises.

- Licensed Florida cash buyer

- Close in 7-21 days, on your timeline

- Free, no-obligation cash offer

- We respond within 24 hours

Cash Buyers Network

Sources & References

External sources cited in this article. Verify current figures and rules directly with the issuing source — Florida real-estate data and program rules change quarterly.

- uncovers outstanding code violationsdufaultlaw.com

- $0.70 per $100flatfeemlssells.com

- Sellers pay in South Florida countiesgulfcoastregroup.com

- Buyers typically pay 2%–5%houzeo.com

- 0.20% of the loan amountinvesteamrealty.com

- Cash to close equals closing costs plus your down paymentpegasuslends.com

- Cash buyers may also receive a net creditteamhawley.com

From the Blog

Continue Reading

home-selling

Inheritance Property Options: Your 2026 Heir's Guide

Explore inheritance property options in 2026: sell, rent, or move in. Learn how each choice impacts your finances and tax obligations.

Read articlehome-selling

Pitfalls of Listing Inherited Homes: 2026 Guide

Discover the pitfalls of listing inherited homes in 2026. Learn key strategies to navigate probate and safeguard your estate's value.

Read articlehome-selling

Seller Financing Rental Property in Florida: 2026 Guide

Discover how seller financing rental property in Florida can unlock investment opportunities. Learn the benefits, requirements, and legal steps.

Read articlehome-selling

Role of Heirs in Property Sales: 2026 Guide

Discover the role of heirs in property sales. Learn when you can sell inherited property and avoid common probate mistakes.

Read articleFrequently Asked

Common Questions

What are closing costs in Florida?

+

Closing costs in Florida are the fees, taxes, and prepaid expenses paid by buyers and sellers to complete a real estate transaction. Buyers typically pay 2%–5% of the purchase price, while sellers pay 6%–10%.

Who pays closing costs in Florida, the buyer or the seller?

+

Both parties pay closing costs, but for different items. Sellers pay the deed documentary stamp tax and agent commissions. Buyers pay mortgage taxes, title fees, and loan charges. Some costs are negotiable between parties.

Do cash buyers pay closing costs in Florida?

+

Cash buyers pay reduced closing costs because they avoid Florida's mortgage documentary stamp tax and intangible tax. They still pay title fees, the deed tax credit, and any negotiated costs, but their total is significantly lower than a financed buyer's.

What is the difference between closing costs and cash to close?

+

Closing costs are the fees and taxes due at closing. Cash to close is the total funds you must wire, which includes closing costs plus your down payment, prepaid insurance, escrow deposits, and prorated taxes, minus any earnest money already paid.

Can closing costs be negotiated in Florida?

+

Several closing costs are negotiable, including who pays owner's title insurance, seller concessions toward buyer costs, and settlement service fees. State-mandated taxes like documentary stamp and intangible taxes are fixed by law and cannot be negotiated.