How to Handle an Urgent Home Sale in 2026

Learn how to handle an urgent home sale effectively in 2026. Master key steps to maximize equity and avoid financial disaster today!

What are the first critical steps to handle an urgent home sale?

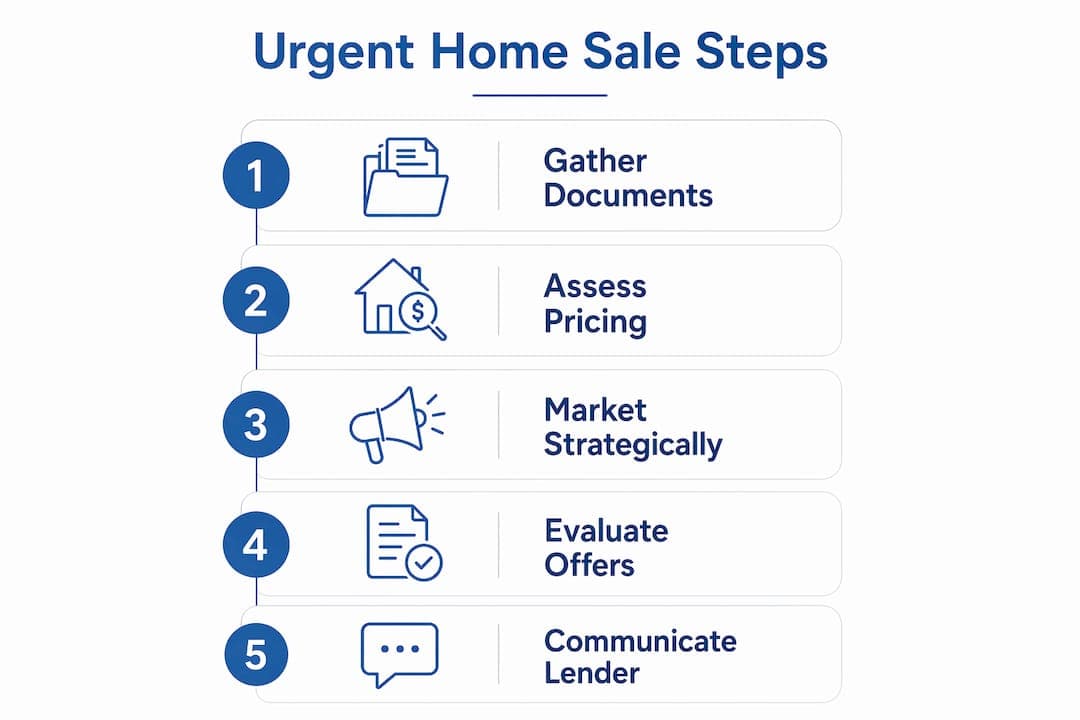

- Step 1 — Gather your mortgage statements, deed, property tax records, and any foreclosure notices. Place them in a single folder, physical or digital You will reference these documents in every conversation going forward.

- Step 2 — Call your mortgage servicer and use the exact phrase "loss mitigation." This language transfers your file to a specialized department with authority to pause foreclosure proceedings A standard customer service rep cannot do what a loss mitigation officer can.

- Step 3 — Document every call. Write down the date, time, representative's name, and a summary of what was said This paper trail can be the difference between keeping your options open and losing them.

- Step 4 — Set your financial priority clearly. Decide whether your goal is maximum speed, maximum sale price, or maximum debt relief These three goals require different strategies, and conflating them wastes time you do not have.

- Step 5 — Request all communications in writing. Ask your servicer to confirm any verbal agreements by email or certified mail.

Key Takeaways

- Triage first, list second

- Gather all mortgage and legal documents within 24 hours

- Price below market from day

- Competitive pricing plus a first-weekend showing blitz

- Use "loss mitigation" language

- This exact phrase routes your lender call to the right

- Compare at least three cash

- Even under time pressure, a short comparison window

How to price and market your home for a fast sale

Accurate pricing from day one is the single most effective selling home fast tip available in the 2026 market.

Accurate pricing from day one is the single most effective selling home fast tip available in the 2026 market. Homes average 47 days on market in 2026, with additional delays from inspections, appraisals, and buyer financing. For an urgent seller, that timeline is unacceptable unless you price and market aggressively from the start.

Data-driven pricing combined with concentrated showings is the most effective quick-sale playbook available. A first-weekend showing blitz creates urgency among buyers and generates competing offers, which protects your net proceeds even at a lower list price. Professional photography is not optional here. Listings with high-quality images attract significantly more online views, and in a compressed timeline, every day of buyer attention counts.

Overpricing is the most common and costly mistake urgent sellers make. Homes that linger on market develop a stigma that actively discourages buyers. Buyers assume something is wrong with a property that has sat for weeks, and that assumption is nearly impossible to reverse without a dramatic price cut that signals desperation.

Pro Tip: Build your pre-listing buzz before the property goes live. Share teaser photos with your agent's buyer network and on social media three to five days before the official listing date. Early interest creates a sense of competition that accelerates offers.

For Florida-specific timing and market data, the Florida real estate trends resource from Housefastcashfl offers current context on Sun Belt market conditions that directly affect your pricing decisions.

What quick-sale options can speed up an urgent home sale?

- — Cash buyers: Cash offers close fastest but typically come in below market value because the buyer absorbs repair costs and transaction risk. The upside is certainty. No financing contingencies, no appraisal delays, and closing timelines as short as four to seven days are realistic. Always require proof of funds before signing anything.

- — iBuyers (such as Zillow Offers or Opendoor): These platforms provide fast digital offers but charge service fees that can reach 5–8% of the sale price. They also require properties to meet condition thresholds, which disqualifies many distressed homes.

- — Short sales: If your home is worth less than what you owe, a short sale requires lender approval to accept less than the full mortgage balance. The process takes 60–120 days on average but can preserve your credit better than foreclosure. It is not a fast option, but it is a legitimate one.

- — Auctions: Auction timelines are fast, but reserve prices are often set low to attract bidders. You may net less than a negotiated cash sale. Auction fees also reduce your proceeds.

How to communicate and negotiate with your lender

- Step 1 — Call your servicer and state explicitly: "I am experiencing financial hardship and I am requesting a loss mitigation evaluation." Using this exact language triggers a mandatory review process under federal mortgage servicing rules.

- Step 2 — Request the complete loss mitigation application package by both email and certified mail Having it in writing protects you if the servicer later claims no request was made.

- Step 3 — Ask for a single point of contact. Repeat storytelling to different representatives wastes time and creates inconsistencies in your file.

- Step 4 — Follow up every 7 to 10 days. Frequent documented contact keeps your application active and prevents file closure before your foreclosure deadline.

- Step 5 — Confirm every verbal agreement in writing within 24 hours of the call.

What common obstacles arise in urgent home sales?

- — Overpricing: A home priced above comparable sales will sit. Every week on market reduces your leverage and signals distress to buyers. Price accurately from day one, not after two weeks of silence.

- — Inspection surprises: Pre-inspections reduce renegotiations and prevent deal collapses. Spending $300 to $500 on a pre-listing inspection identifies issues before buyers use them as leverage. Fix what you can and disclose the rest upfront.

- — Buyer financing failure: A buyer with a pre-approval letter is not a guaranteed buyer. Ask your agent to assess the strength of the pre-approval before you accept an offer. Cash buyers eliminate this risk entirely.

- — Contingency chains: If a buyer needs to sell their own home first, that contingency can delay your close by 30 to 60 days. In an urgent sale, avoid accepting offers with home-sale contingencies unless no better option exists.

- — Showing inflexibility: Restricting showing hours reduces your buyer pool. In an urgent timeline, accommodate every reasonable showing request, including evenings and weekends.

Key takeaways

Handling an urgent home sale successfully requires immediate documentation, accurate pricing, and active lender communication from day one, not after options have expired.

Handling an urgent home sale successfully requires immediate documentation, accurate pricing, and active lender communication from day one, not after options have expired.

What I've learned from watching urgent sales succeed and fail

— Eric

What I've learned from watching urgent sales succeed and fail

After years of working with homeowners in foreclosure, inheritance situations, and sudden financial hardship, the pattern is consistent.

After years of working with homeowners in foreclosure, inheritance situations, and sudden financial hardship, the pattern is consistent. The sellers who come out ahead are not the ones with the best properties or the most time. They are the ones who got organized on day one and stayed organized throughout.

The biggest mistake I see is sellers who spend the first two weeks in denial, hoping the situation will resolve itself, and then scramble when the foreclosure clock is already deep into its countdown. By that point, options like short sales or loss mitigation workouts are often off the table. The window closes faster than most people expect.

Balancing speed and price is genuinely hard in a 2026 market where days on market are longer than sellers anticipate. My honest advice is this: if you need to be out in 30 days or less, a cash buyer is almost always the right call, even if the number is lower than you hoped. The certainty of a closed deal beats the uncertainty of a traditional listing every time when the stakes are this high.

Get professional help early. Whether that is a real estate attorney, a HUD-approved housing counselor, or a vetted cash buyer, outside expertise pays for itself. And if you are dealing with an inherited property, the legal and tax complications add another layer that most sellers are not equipped to handle alone. Resources like the inherited property guide can clarify what you are actually dealing with before you commit to a path.

Stay calm, stay organized, and move fast. Your mindset in the first 72 hours sets the trajectory for everything that follows.

Housefastcashfl can help you close fast and confidently

Housefastcashfl works with Florida homeowners facing foreclosure, inherited properties, and damage-related sales every day.

Housefastcashfl works with Florida homeowners facing foreclosure, inherited properties, and damage-related sales every day. The process is straightforward: submit your property details, receive a no-obligation cash offer within 24 hours, and close in as few as four days with no repairs, no commissions, and no showings required. If you want to understand whether a cash buyer is the right fit for your situation, the legitimate cash buyer guide walks you through exactly what to look for. For sellers focused on maximizing their proceeds under time pressure, Housefastcashfl offers transparent, fair offers backed by Google and BBB verification.

Side-by-side comparison

| Traditional listing | Urgent sale approach | |

|---|---|---|

| Pricing strategy | List at or above market, reduce later | Price 3–5% below comparable sales on day one |

| Showing schedule | Flexible, ongoing | Concentrated first-weekend open house blitz |

| Photography | Standard listing photos | Professional photography plus pre-listing teaser content |

| Negotiation posture | Hold firm on price | Offer repair credits instead of price reductions |

| Timeline expectation | 47+ days average | Target 14–21 days with right buyer pool |

Free Cash Offer

Ready to sell your house for cash?

Tell us about your property. We'll come back within 24 hours with a fair, no-obligation cash offer — no commissions, no inspection drama, no closing-cost surprises.

- Licensed Florida cash buyer

- Close in 7-21 days, on your timeline

- Free, no-obligation cash offer

- We respond within 24 hours

Cash Buyers Network

Sources & References

External sources cited in this article. Verify current figures and rules directly with the issuing source — Florida real-estate data and program rules change quarterly.

From the Blog

Continue Reading

home-selling

Inheritance Property Options: Your 2026 Heir's Guide

Explore inheritance property options in 2026: sell, rent, or move in. Learn how each choice impacts your finances and tax obligations.

Read articlehome-selling

Pitfalls of Listing Inherited Homes: 2026 Guide

Discover the pitfalls of listing inherited homes in 2026. Learn key strategies to navigate probate and safeguard your estate's value.

Read articlehome-selling

Seller Financing Rental Property in Florida: 2026 Guide

Discover how seller financing rental property in Florida can unlock investment opportunities. Learn the benefits, requirements, and legal steps.

Read articlehome-selling

Role of Heirs in Property Sales: 2026 Guide

Discover the role of heirs in property sales. Learn when you can sell inherited property and avoid common probate mistakes.

Read articleFrequently Asked

Common Questions

What does "loss mitigation" mean in a home sale?

+

Loss mitigation is the formal process through which a mortgage servicer evaluates alternatives to foreclosure, including loan modifications, short sales, or repayment plans. Requesting it by name routes your file to a specialized department with authority to pause foreclosure proceedings.

How fast can you realistically sell a house in an urgent situation?

+

Cash buyers can close in as few as four to seven days. Traditional listings in 2026 average 47 days on market, making them a poor fit for most emergency home sale situations without aggressive pricing and marketing.

Is a short sale better than foreclosure for my credit?

+

A short sale typically causes less credit damage than a completed foreclosure and may allow you to qualify for a new mortgage sooner. It requires lender approval and takes 60 to 120 days, so it is not a fast solution.

How do I verify a cash buyer is legitimate?

+

Request proof of funds in writing, ask for a clear fee disclosure with no upfront charges, and check the buyer's Google reviews and BBB rating. Housefastcashfl provides a detailed vetting checklist for Florida sellers.

Should I make repairs before an urgent sale?

+

For most urgent sellers, a pre-inspection to identify issues is worth the cost, but completing major repairs is not. Offer repair credits at closing instead. Cash buyers typically purchase properties as-is, eliminating the repair question entirely.