Property Sale Process Florida: Your Fast Cash Guide

Navigate the property sale process Florida with our fast cash guide. Sell quickly despite challenges and move forward in days!

Understanding the Florida property sale landscape

- Listing and showings: Days to weeks before a serious offer arrives.

- — Offer negotiation: Buyer financing pre-approval review, which can take 5 to 10 days.

- — Earnest money deposit: Typically 1 to 3 percent of the purchase price, due within 3 days of contract execution.

- — Inspection period: Usually 10 to 15 days, during which buyers can cancel for nearly any reason.

- Appraisal: Required by most lenders, adding another 7 to 14 days.

Key Takeaways

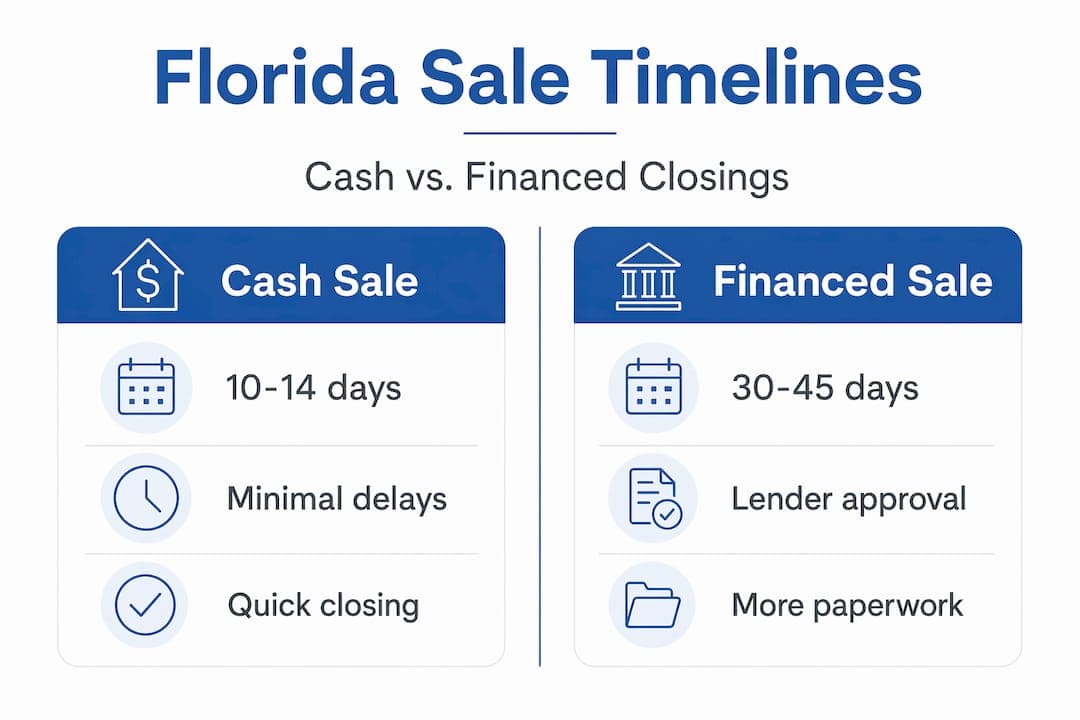

- Cash sales are fastest

- Selling a property for cash can close in as little as 10 to

- Legal document readiness

- Ensure your deed and disclosures meet Florida requirements

- Foreclosure has court

- Foreclosure processes follow strict judicial timelines that

- Prepare closing paperwork

- Gather payoff info, ID, and communicate with your closing

Key legal and procedural steps in a Florida property sale

- Step 1 — Prepare a compliant deed. Under Florida Statute 689.02, every deed must be in writing, include the full legal names of both parties, contain the property's legal description, carry the seller's signature, and be notarized before it can be recorded with the county clerk A typo in the legal description can void the transfer entirely.

- Step 2 — Complete the seller disclosure notice. Florida law requires sellers to provide written disclosure of known material defects before or at contract signing If you deliver this late, the buyer gains the right to cancel the contract within three days of receiving it, regardless of how far along the sale is.

- Step 3 — Clear title issues. Any outstanding liens, judgments, or code violations attached to the property must be resolved or formally addressed before closing Your title company or closing attorney handles the search, but you need to act quickly when issues surface.

- Step 4 — Execute the purchase agreement. Both parties sign a Florida Realtors or custom contract Review all deadlines carefully because each date is contractually binding.

- Step 5 — Coordinate title insurance. Florida closings almost always require title insurance to protect the buyer and lender from prior ownership claims Cash buyers often still require it.

Step-by-step guide to a fast cash sale in Florida

- Step 1 — Gather your ownership documents. Pull your deed, most recent mortgage statement, HOA documents if applicable, and any open permits or code violations Having these ready before you contact a buyer shaves days off the process.

- Step 2 — Get a cash offer. Reputable cash buyers in Florida deliver offers within 24 hours of reviewing basic property information No photos required, no inspection contingency.

- Review and execute the purchase contract. Read every deadline — Key dates include the title search period, any inspection window (cash buyers often waive this), and the scheduled closing date.

- Step 4 — Open title and order payoff. Your closing agent orders the title search and requests a payoff statement from your lender simultaneously This parallel processing cuts days off the timeline.

- Step 5 — Review your Closing Disclosure. Federal law gives you three business days to review this document before closing Use this time to verify every number, especially the payoff figure and net proceeds calculation.

Common pitfalls and verification steps to ensure a smooth closing

- — Stale payoff figures: Payoff statements expire quickly, sometimes in 10 days. If your closing gets rescheduled, request a new one immediately.

- — ID mismatches: Your name on the deed must match your government-issued ID exactly. Even a middle initial difference can require a court-filed affidavit to resolve.

- — Outstanding permits: Unpermitted work discovered during the title search can halt closing entirely until resolved with the county.

- — Unpaid HOA balances: Florida law gives HOA liens priority status. Your closing cannot proceed until the balance is settled.

- — Late disclosure delivery: Handing the seller disclosure notice to the buyer after contract signing, without their acknowledgment, resets their cancellation window.

Why understanding court-driven timelines beats informal promises in urgent Florida sales

Here is something most sellers learn the hard way: no attorney, no buyer, and no investor can override the court's calendar.

Here is something most sellers learn the hard way: no attorney, no buyer, and no investor can override the court's calendar.

When a foreclosure lawsuit is active, the timeline belongs to the judge and the clerk, not to you or the person you're negotiating with. We've seen homeowners delay a cash sale because an informal promise from a lender's loss mitigation department made them believe they had more time than they actually did. Then the auction date posts, and that promise means nothing because the court auction schedule does not accommodate private negotiations.

Florida's judicial foreclosure process is inflexible by design. Once a summary judgment is entered, the only things that can stop the auction are a formal court order, a filed bankruptcy petition, or a completed sale that closes and funds before the auction date. A handshake deal doesn't appear on the court's docket.

This is why we push homeowners to act at the lis pendens stage, not after the judgment is entered. Once lis pendens is filed, you typically still have several months before an auction is set. That is your real window. Waiting to see if the lender will "work with you" informally can burn that window completely.

The professionals who help sellers most in these situations are the ones who understand court rules cold and can build a foreclosure sale planning timeline around hard legal deadlines, not optimistic estimates. If you're working with anyone who gives you a timeline without referencing the specific court dates in your case, get a second opinion.

Realistic planning, built on statute and court schedule, is what protects your equity and your options. Everything else is noise.

How we simplify your fast, cash property sale in Florida

If you need expert help to execute a quick cash sale, here's how our service can support and simplify your journey.

If you need expert help to execute a quick cash sale, here's how our service can support and simplify your journey.

Sell my house fast Florida with a process built specifically for homeowners under pressure. Whether you're facing foreclosure, storm damage, or an inherited property you can't maintain, we deliver a no-obligation cash offer within 24 hours and can close in as few as four days. No repairs, no showings, no financing contingencies that fall through at the last minute.

We guide you through every document, coordinate with your closing agent, and handle the complexity so you don't have to. Our buyers are verified, legitimate home buying companies with a track record you can confirm through Google and BBB listings. If you need to sell before foreclosure, we know exactly how to build a closing timeline around your court deadlines. Reach out today and take back control of your situation.

Side-by-side comparison

| Typical timeline | Key bottleneck | |

|---|---|---|

| Financed (conventional) | 30 to 45 days | Lender underwriting and appraisal |

| FHA/VA loan | 45 to 60 days | Additional inspection requirements |

| Cash sale | 10 to 14 days | Title work and payoff verification |

| Distressed cash sale | As few as 4 to 7 days | Document readiness |

At-a-glance comparison

Pre-foreclosure cash sale — Timeline: 7 to 14 days · Equity protection: High (you control price) · Auction risk: None Short sale —…

Pre-foreclosure cash sale — Timeline: 7 to 14 days · Equity protection: High (you control price) · Auction risk: None

Short sale — Timeline: 60 to 120 days · Equity protection: Low (lender controls) · Auction risk: Eliminated if approved

Foreclosure auction — Timeline: Court-scheduled · Equity protection: None · Auction risk: Total loss possible

Loan modification — Timeline: 30 to 90 days · Equity protection: Maintained if approved · Auction risk: Paused during review

Free Cash Offer

Ready to sell your house for cash?

Tell us about your property. We'll come back within 24 hours with a fair, no-obligation cash offer — no commissions, no inspection drama, no closing-cost surprises.

- Licensed Florida cash buyer

- Close in 7-21 days, on your timeline

- Free, no-obligation cash offer

- We respond within 24 hours

Cash Buyers Network

Sources & References

External sources cited in this article. Verify current figures and rules directly with the issuing source — Florida real-estate data and program rules change quarterly.

From the Blog

Continue Reading

home-selling

Red Flags When Selling Property: 2026 Seller's Guide

Discover the red flags when selling property in 2026. Protect your equity and avoid pitfalls with our essential seller's guide!

Read articlehome-selling

Florida Landlord Tenant Law: Selling With Tenants

Learn about Florida landlord tenant law sale rules. Discover your legal obligations when selling tenant-occupied properties and protect yourself.

Read articlehome-selling

What Is a Fast Closing? a Real Estate Guide for Sellers

Discover what is a fast closing in real estate. Learn how sellers can sell quickly and maximize cash when time is critical.

Read articlehome-selling

What Is a No-Obligation Offer? a Homeowner's Guide

Discover what is a no-obligation offer and learn how it empowers homeowners in real estate decisions. Gain clarity without commitment!

Read articleFrequently Asked

Common Questions

How fast can I sell my Florida home for cash?

+

Cash sales in Florida close in as little as 10 to 14 days because they skip lender underwriting entirely. With all documents ready upfront, some closings complete in as few as four days.

What legal documents are required to transfer property in Florida?

+

You need a written deed that includes the full legal property description, seller's signature, and notarization, then recorded with the county clerk per Florida Statute 689.02 to legally complete the ownership transfer.

Can I stop a foreclosure sale if I pay the overdue amount?

+

Florida allows you to redeem the property by paying all arrears and costs, but only until the clerk files the certificate of sale immediately after the auction. Once that document is filed, redemption is no longer an option.

What happens if I miss mortgage payments and foreclosure starts?

+

Your lender sends a breach letter giving you 30 days to catch up before filing a lawsuit, and once sued, you have 20 days to respond in court. Acting before that lawsuit is filed gives you the most options.

What should I bring to the closing for a Florida property sale?

+

Bring a government-issued photo ID, all keys and garage remotes, any appliance manuals, property warranties, and the property survey if you have it available.